After finishing this short reading you’ll be able to wisely choose both the rate and the financial institution for your next loan.

Misinformation about types of interest rates is dangerously spread out there. So pay close attention to the following so none will be able to screw you over.

CALCULATE YOUR MONTHLY RATE

To be able to compare the different rates, you have to calculate the monthly rate.

There are several types of interest rates. Let’s discuss three of them:

Monthly Interest rate: This is the rate that is calculated over your entire debt amount every single month. This type is pretty clear, you already know the % of monthly interest.

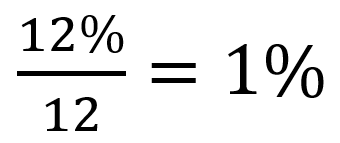

APR (Annual Percentage Rate): To convert it to a monthly rate, you have to divide by 12. For example, a 12% APR converted to month is 1%:

APY (Annual Percentage Yield, also know as EAR): To convert it to a monthly rate, you have to discount it (the opposite of compounding). This formula is more complex:

Taking as an example a 12% APY, the monthly rate is the following:

As you can see, if you convert APR and APY to monthly rate you get different results. For more information visit Investopedia.

Here you have a calculator of loan payments made in Power BI. Feel free to change the input variables to suit your needs.

Note:Power BI has an annoying bug, sometimes it rounds up the input variable to a close number. However, even if the input variables are not 100% accurate to your needs, the results are pretty close to the monthly payments you are going to run into.

Note: “Insurance and Fees” input variable is not considered to be subject to interest rates. Ask your financial institution if this is your case

Compound Interest refers to taking advantage of time to build up your wealth.

Also known as interest on interest, as time passes, your initial investment has some returns. Those investment’s returns can be invested again, bringing up your total wealth to: initial investment + investment’s return.

Later on, you can take the return of your current assets (initial investment + initial investment’s return) and invest it back, creating a never-ending process.

RUNNING THE NUMBERS

Let’s suppose you invest $100 at a 10% annual interest rate. When the year ends, those $100 would’ve accrued to $110. The art of compound interest is taking that money and reinvesting it again, in this case, those $110.

Another way of interpreting compound interest is by watching how a stock’s price increases. If a stock’s value increases at a pace of 10% annually, it means that every year it’ll be 10% more expensive.

RUNNING THE NUMBERS

Corp A Inc. has a stock that is worth $100. After the first year (if the annual yield is 10%), its price will be $110. However, by the end of the second year, it’ll be worth $121 ($110 x 110%).

POWER BI RUNS THE NUMBERS FOR YOU

Try running your number by yourself in this Power BI report! Input your initial investment, the interest rate, and you can also take into consideration yearly cash flows.

Do you recall part I and II blog posts saying that the S&P 500 index has had an average annual return of about 8%? Well, that’s part true.

When you earn interests over your investments (bonds, stocks, ETF or even real estate) you must pay taxes.

So, if you invested for a year in an index fund that replicates the S&P 500, and the yield was 10% for that year, you wouldn’t receive the full 10% return.

If you were in Italy, you’d have to pay 26% on taxes, reducing the return rate from 10% to 7,4%.

In the U.S. the tax burden works differently for investments: depending on your federal tax bracket, you would have to pay from 10% to 39,6% on taxes, plus the state tax.

Important: Remember asking your financial institution how much the return of your investment actually is after taxes. They tend to forget that huge detail, on purpose.

A portion of your investment’s return taken by the government

Inflation

Inflation is the increase in cost of living.

While this is a tangible reality for Argentine citizens (Nashdaq article) since they are going to face a 40% inflation rate in 2020, for other countries, it appears not to exist.

In the U.S., the average inflation rate has been around 2% in recent years. Therefore, it’s not as easy to perceive the increase in the cost of living as in Argentina.

Inflation rate is a devour of our investments’ returns.

If you wanted to have the same purchase power in Argentina with the same amount of pesos (currency in Argentina) in a year, you would have to aim at a 40% return investment.

With abnormal high inflation, money could be worthless

For the U.S., in order to keep up with the inflation rate, you need a 2% annual return investment.

Going back to the hypothetical 10% return on the S&P 500, you would really have an 8% return, due to inflation rate.

It’s more than a little ironic that if you decide to invest in the U.S. treasury bonds, due to their extremely low yield, you will still lose money. Check the number at the official site: Treasury.

There’s still salvation

Every disease has its cure, so let’s try to figure out how to tackle taxes and inflation.

Inflation: Invest in a strong currency that is less likely to be devalued, like euros €.

Taxes: Invest in tax-free bonds like government bonds or in a retirement account.

Investing in government’s debt is not as bad as you think

That’s right! Governments like putting their own interests first. Depending on the country, investors on the government’s debt don’t pay taxes.

In Italy, if you invested in government’s securities instead of any other security, you would pay 12,5% on taxes instead of 26%.

In the U.S., investing in Treasury securities (debt instruments issued by the United States Department of the Treasury) is entirely tax free.

Therefore, before comparing any investment option against government’ securities, remember that taxes play a BIG role.

A great retirement account feature

Another possibility to avoid paying big percentages on taxes is investing in retirement accounts. For instance: 401(k) or Roth IRA for the U.S. or fondo pensione for Italy.

Depending on the country, it’s possible to totally avoid paying taxes as long as your investments are in a retirement account.

In Italy you could pay as little as 9% on taxes if you opted for retaining your investment for more than 30 years on the retirement account.

Tax deduction totally depends on your country, so be sure to check that out before considering investing outside of your tax-shelter retirement account.

Paying debt first

As crazy as it could sound, paying your debt first could be an investment.

Not only because having debt increases your interest rate for future loans, but also because taxes don’t apply to debt repayment.

Practical example: Would you rather pay your debt that has an annual 9% interest rate? Or would you invest that money in a fund with a 10% yield?

The 10% yield will be shrunk to 8% if you had to pay 20% on taxes, leaving you with a final yield of 8%. On the other hand, since debt repayment doesn’t pay taxes, your money would have a better use by repaying the 9% interest rate debt.

This also applies to mortgages. Even better: you can get your mortgage interest rate deducted from your annual taxes.

Looking beyond the yield

Sometimes we can find ourselves chasing after the strongest performing investment, overlooking simpler investments.

However, there are other factors, besides risk, that need to be considered: taxes, inflation, commissions, fees, etc.

Financial institutions will hide these factors from you unless you ask. So, next time remember asking for any hidden consideration that could hinder your investment’s return.

This is the end of this series of blog posts.

I hope you liked all the three articles and that you learned something about investments from them.

This website uses cookies to improve your experience. We'll assume you're ok with this, but you can opt-out if you wish. Cookie settingsACCEPT

Privacy & Cookies Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these cookies, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may have an effect on your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.